Collector Penalties

7 min read

Luckily for consumers, financial policy violations come with real

penalties for creditors. The biggest creditors have all been hit with these penalties

(think Wells Fargo, Bank of America). Familiarizing yourself with your rights and what

constitutes a violation can go a long way in protecting your financial interests.

TILA:

Truth in Lending Act

To assure a meaningful disclosure of credit terms, TILA requires creditors to provide

consumers with a uniform system of disclosures that clearly and concisely informs

consumers of their credit terms.

CFPA:

Consumer Financial Protection Act

Section 1036(a)(1)(B), 12 U.S.C. 5536(a)(1)(B)

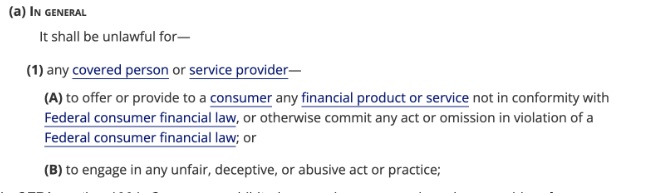

In CFPA section 1031, Congress prohibited covered persons and

services providers from committing or engaging in unfair,deceptive, or abusive acts or

practices in connection with the offering or provision of consumer financial products or

services.

FDCPA:

Monetary and Non-Monetary Damages

- Damages for physical distress - one can recover the costs of treatment from the

collector

- Damages for emotional distress

- Lost wages recovered - if the collector is calling at place of employment and it

has in any way affected their wages, then the debtor can ask for the wages to be

awarded to them

- Statutory Damages for up to $1,000 - the court can award these damages if the

consumer proves the collector violated the FDCPA, but the consumer does not have

to prove that the violation caused any harm. This $1,000 is per lawsuit - not

per violation - so if the creditor violates the FDCPA once or multiple times,

the consumer still only collects up to $1,000.

This includes:

- Repeated phone calls

- The use of abusive or profane language

- Calling during prohibited times

- Threatening or using violence

- Contacting a third party about your debt

- Contacting you at work

- Lying or misleading you about your debt

- Failing to provide verification of your debt

- Failing to identify themselves as a debt collector

- In addition to awarding a consumer monetary damages, a court can

also order the debt collector to cease certain activities—this is called

"injunctive relief." For example, the court can require that:

- Debt collector stop calling

- Debt collector stop sending letters

- Any family members, coworkers, or friends of a debtor who has been affected by

the third party debt collector can also sue for damages (up to $1,000)

TCPA:

https://www.fcc.gov/sites/default/files/tcpa-rules.pdf

- A consumer can recover up to $500 for each violation of the Do Not Call

Registry.

- Up to $500 per violation, and up to $1,500 per violation if the consumer can

show that the TCPA was violated knowingly and willfully.

- There isn’t a maximum cap on these violations, unlike FDCPA violations.

- The statute of limitations for TCPA cases is four years.